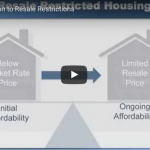

Shared Equity Resale Formulas

Most inclusionary housing programs use resale restrictions to ensure that whenever a home is resold during the affordability period, it is sold at an affordable price. While programs use different resale formulas, most programs seek to balance two goals: allowing the homeowner to benefit from some price appreciation in order to accumulate wealth; and keeping resale prices affordable for subsequent low- and moderate-income homebuyers.

The choice of resale formula has implications for advancing racial equity. Homeownership has traditionally been a main method of wealth-building for American households. Yet Black, brown and other homeowners of color have not realized the same gains as White households, due to both systemic exclusion from homeownership and lower gains in property values. Inclusionary housing programs can put homeownership opportunities in reach for low-income households of color.

Different programs give different priority to wealth accumulation and affordability preservation, depending on local market conditions and the characteristics of targeted households and/or neighborhoods.

A program that uses a resale formula that provides more equity to the seller upon resale (placing greater emphasis on wealth-building) runs the risk that significant additional subsidy could be needed to help keep the home affordable to the next buyer, or that without additional subsidy the home may lose affordability. On the other hand, a program that uses a resale formula that keeps more of the appreciation in the home (placing greater emphasis on long-term affordability) provides less wealth-building opportunity for each individual homeowner. Priorities should be informed by feedback from local racial equity organizations and people of color.

Twin Cities Habitat for Humanity* has a resale formula that places greater emphasis on wealth-building. Under their shared equity formula, the share of appreciation that the homeowner receives increases for every year that they own the home.

San Mateo, CA’s Below Market Rate (Inclusionary) Program uses an AMI-based formula, where the resale price is based on the change in Area Median Income. This formula places greater emphasis on long-term affordability.

Index Formulas

One popular approach to setting a resale price is the index-based formula. Typically the program will set the resale price equal to the original affordable purchase price plus a set rate of appreciation tied to changes in area median income (AMI) or the consumer price index (CPI).

Washington, DC, calculates the change in AMI based on a 10-year rolling average, which helps prevent a situation in which a homeowner would have to sell at a loss due to a short-term dip in AMI or sell at a price that is unlikely to allow the subsequent homeowner any price appreciation because of a short-term spike in AMI.

The AMI-based appreciation model is one of the most intuitive approaches from a long-term affordability perspective, as it ensures that the home price will still be affordable to the same targeted income group in the future. The AMI-based index formula does not, however, ensure that basic homeownership cost assumptions will remain constant over time.

Fixed-Percentage Formulas

Some jurisdictions use a fixed-percentage formula whereby the resale formula is determined by adding a pre-determined percentage increase to the original purchase price each year. This approach is simpler to explain to potential homebuyers and affords homeowners greater certainty about what to expect at the point of resale.

Park City, Utah allows an annual appreciation rate of 3 percent, though if market values in the city appreciate less than 3 percent annually, the inclusionary homeowner is limited to the rate of citywide market appreciation.

Boulder, Colorado uses a hybrid approach in an attempt to strike the right balance in their community. The program ties the resale price to an annual appreciation factor based on whichever index—the AMI or CPI—grew at a lower rate over the ownership period, but it also caps the price increase at 3.5 percent.

Appraisal Based Formulas

Burlington, Vermont, Chicago, llinois, Santa Fe, New Mexico, and Chapel Hill, North Carolina use appraisal-based (market-appreciation) formulas. Under this structure, the resale price is set based on the original price plus a percentage of the difference between the home’s original appraised value and the appraised value at the time of resale. Localities often set limits on the maximum allowable appreciation. In Burlington, for example, the resale price can be increased by 25 percent of the home’s market appreciation (as determined by appraisals).

In most cases, programs also allow the homeowner to increase the resale price to reflect the value of major repairs or other permitted improvements made by the homeowner during ownership, which helps to maintain the quality and condition of the affordable housing stock.

This type of formula is most tied to the housing market, which means it is also affected by the systemic racism inherent in the housing market. For example, homes in neighborhoods where the population is predominantly people of color have been shown to appreciate less than comparable homes in neighborhoods where the population is mostly White. This type of formula is also less predictable than other formulas. Partly for these reasons, many jurisdictions are moving toward a fixed-percentage formula.